Press Room

This is the Neolink blog. Get the latest news and insights on global logistics, emerging technologies and what’s happening on the ground at Neolink.

Want to know more?

Explore our site.

Want to know more?

Explore our site.

NEOLINK H1 2021 REVIEW – How did we get here and where to now for Australia’s Global Supply Chains?

Thursday 14th of July 2021

INTRODUCTION

Since the beginning of 2020; Global and Local Supply Chains have been on the COVID 19 rollercoaster – shipping and consumption dropping 13% one minute and in double digit growth the next, in an industry where typically 2% to 3% shifts annually on any data point are the norm.

Whether it is ocean freight rates, local terminal fees, consumer demand, factory production, sailing schedule reliance, empty yard fees, warehousing costs – fundamentally all these areas have experienced >10% shifts in the past 12 months and have driven changes in landed unit costs, pricing, profit margins and will inevitably lead to inflation, which Australian consumers will feel in the coming months/years ahead if they haven’t felt it already.

In this H1 Review we have attempted to synthesize all of the information and data available to provide a clear view in order to help our customers communicate the impact COVID has had on global supply chains with your customers and what this means for all industries moving forwards for the rest of 2021 and beyond.

COVID IMPACT ON CONSUMER DEMAND & INDUSTRY

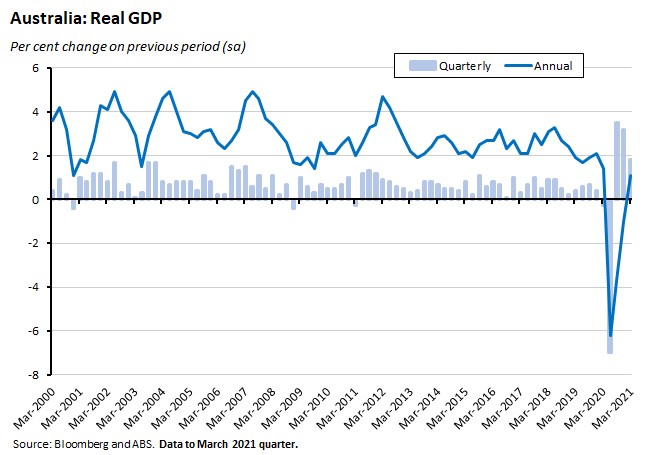

Household consumption is typically one of those very boring data points that largely never changes QTR to QTR, Month to Month and Year to Year here in Australia, as well as other developed western economies. Anything close to a 2% real GDP change was a walk on the wild side, and even the Global Financial Crisis saw a very minimal drop in Quarterly GDP here in Australia and should give context to the impact of COVID 19.

Please see below the -8% drop in GDP in the first QTR of 2020 followed by the biggest GDP QTR’s in the past 20 years:

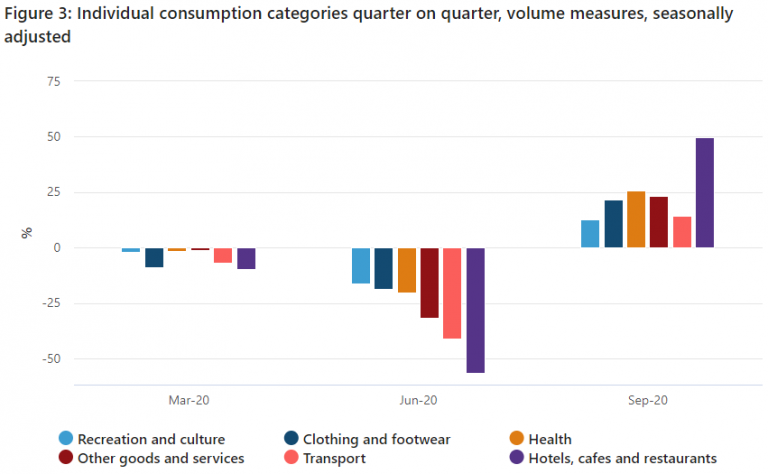

The above/below charts talks to the anecdotal feedback/conversations we have all been having with family, friends, customers, and suppliers since the beginning of the pandemic. Either business is booming or your local café that you get your morning coffee from is no longer in business with Hotels, Cafes and restaurants experiencing the biggest roller coaster of all in the past year.

One minute they are in lockdown with a -50% drop in consumption only propped up by online orders/Deliveroo takeaways and then to be reopened experiencing the biggest growth the industry has had in a QTR for the past 30 years – only to now be locked down again in NSW. See below:

Source: Australian Bureau of Statistics

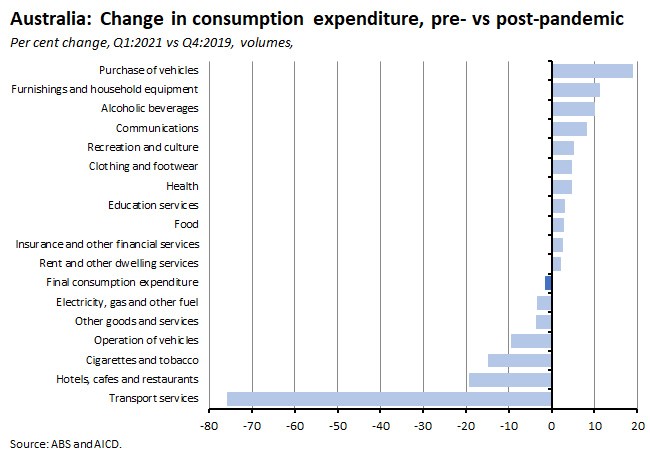

The significant shifts in consumption are the core reason and driver behind why global supply chains have been so significantly impacted by COVID. The World Shipping Council just this week was quoted stating that the Asian exports to the US has grown by 34% and is the highest quarterly gain since records began (i), as a result this increase/shifts in demand on importers/exporters has created “The Perfect Storm” in the global freight market.

In addition to the above since the beginning of the year we have had to contend with two once in a lifetime scenarios with the Suez Canal Blockage and The Port of Yantian Closure. The Suez Canal Blockage in the early hours of March 23rd of this year effectively put a halt for six days to one of the busiest trade routes in the world – with costed to the global economy an estimated $6.7M USD per minute (xii) and lost shipping capacity of 20 to 30% over a period of multiple weeks following the delay. Delays on vessel schedules around the world were impacted and freight prices across the board jumped 278% in March as a result of the blockage according to the FBX.

The month-long closure at one of the busiest ports in the world (The Port of Yantian) due to a COVID outbreak at the end of May was another once in a lifetime event in the shipping industry. NEOLINK were the first Australian Freight Forwarder to break the news on the 26th of May (xiii), due to an unfortunate client shipment that was impacted with its delivery being blocked at the entry of one of the ports terminals. The Yantian impact had a catastrophic impact on rates to Australia – across ports in China the average 40ft container rate to Australia was around the $3,600 USD mark in May and latest rates in July for the second half of the month is showing rates ranging from $6,400 USD up to $7,000 USD per 40ft.

GLOBAL FREIGHT RATE CHANGES & IMPACT ON SUPPLY CHAINS

As per the above, Consumer Demand has significantly outstripped the industry’s ability to meet the supply side of the equation even before the Suez Canal and Yantian Port issues this year – shipping lines don’t have enough services or vessels, terminals are not adequately equipped, and container imbalances have resulted in the highest ocean freight rates on record:

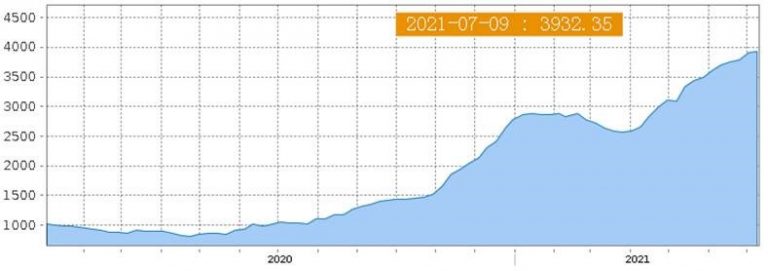

FBX Global Freight Rate Index – July 2019 to July 2021 – Per FEU USD

Shanghai Container Freight Rate Index – 2020 to July 2021 – Per TEU USD

The shipping lines have been the focus of the frustration from the rest of the industry as their profits exceed record levels and calls have been made to regulate prices, with Joe Biden expected to sign an executive order in the coming days to put pressure on these carriers . One of the biggest challenges has been that the industry slumped from 2018 to 2020 prior to the pandemic, which resulted in Maersk (worlds #1 shipping line) as well as the other major shipping lines cutting back on Capital Expenditure to an all-time record low. This ultimately resulted in fewer vessels being ordered or going into production as well as fewer new containers being ordered (iii) adding issues to the supply side of the equation prior to 2020.

LANDSIDE OPERATIONS

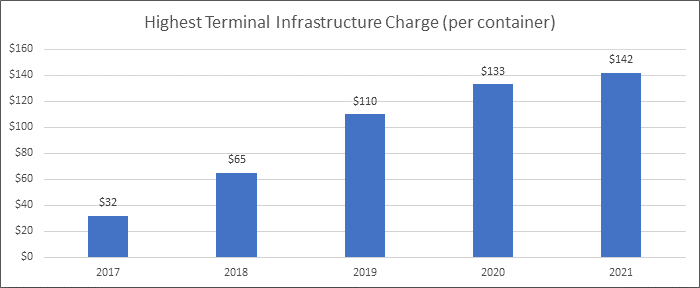

In addition to the shipping lines, landside operations at the major port terminals here in Australia and globally have been significantly impacted with the increase in volume (vi), as well as Scott Morrison famously last year threatening to call in the military on perfectly timed union strikes within the terminals in the height of the pandemic (v). In recent months we can confirm that the MUA has signed new agreements with Hutchinsons and DP World, but are still going through discussions with finalizing an agreement with Patricks. These agreements take average annual salaries at the ports to $170,000 AUD per annum (viii), approx. 283% more than the average Australian income according to the latest data from the Australian Taxation Office (ix).

All of the Australian Port terminal operators (Hutchinsons, DP World, Patricks and VICT) have used the above in recent years to implement new charges called Terminal access fees or Terminal Infrastructure surcharges that have increased from a nominal $30 per container to close to $150 per container this year. This is an additional charge already on top of VBS Fees, port terminal charges and other ocean freight charges, which get ultimately get passed onto importers:

Source xi: Terminal Infrastructure Charges, excludes VBS, Empty Dehire and Local port Charges

Key Areas of Focus and Recommendations Moving Forwards

A consistent theme in all our updates is ensuring we plan as early as possible (especially with Christmas around the corner) and ensuring our customers POs are in our order management system. Please ensure that every time you raise a PO with an overseas supplier we are in CC and engaging our origin offices to start pre booking/communicating with the carriers as well as suppliers. Whilst this does not guarantee a delay won’t occur or a port shutting down operations, it is significantly better than trying to book the week of the cargo being ready. Please plan as early as possible for Christmas.

We have committed that we will not consolidate shipments for commercial benefit in NEOLINK’s interest ahead of our customers, since we have implemented a lot of our workflow automation and Artificial Intelligence capabilities our Customer Operations team are spending more time on the booking part of the supply chain process for all customers individually.

One additional data field we do get from some customers on their purchase orders are RIS dates, which can significantly impact our recommendations and what services we book on. If we know an order is of higher priority this may even result in us recommending an entirely different transport mode altogether i.e., Air Freight if Sea Freight is just not feasible.

Prior to making a booking, NEOLINK and our origin offices are working with the shipping lines to do our best to understand any market forces that can result in booking delays. This is by no means full proof, but we are in control of everything prior to the container being loaded and at the wharf waiting for loading. Once it is on the vessel, we are largely at the mercy of the shipping lines and terminals, which we know are behind schedule and experiencing delays, but try to manoeuvre bookings where we can to reduce the incidence of these events occurring.

NEOLINK for a number of our customers are holding stock in 3PL facilities and are actively encouraging customers to invest/hold more stock to ensure customer deliveries are met where feasible. This is obviously impossible for orders that are either “Made to Order”, “Time specific” or “Just in time” supply chains, but on these customers, we will always ensure we are planning as early as possible.

NEOLINK are working with our customers as best as we can to provide forecasts on costings and rate increases as they come. Ocean Freight rates typically move every fortnight, and we are trying to pre-empt or communicate those increases as soon as possible once released. We have and will also continue to provide USD accounts to customers that want to pay us in USD to mitigate foreign exchange risk – if you don’t have a USD account and would like to be set up, please contact your NEOLINK Customer Ops Coordinator.

On average NEOLINK’s data from over 150 customers & 300+ suppliers is showing an average delay on original Ex-Factory dates of 14 days from the time a PO is placed – so please allow for these delays in addition to any shipping time we provide you. Our team work extremely hard with all our customers to ensure we pre plan and get cargo to Australia as quick as possible, but there are several market forces that are outside of our teams’ control, so please allow for these delays and do not commit to any urgent project without speaking to your NEOLINK Customer Operations contact first.

Sources:

The NEOLINK Team are here to help and assist you during an unprecedented time in modern history as we navigate a market we have never seen before. As such our business has maintained our commitment to continue our overinvestment in technology, automation and artificial intelligence applications to make our team as efficient as possible and enable them to spend more time finding ways to make your supply chain as efficient as possible in return.

If you or any member of your staff have any questions, please don’t hesitate to reach out to any member of the NEOLINK Team.

Best regards,

NEOLINK Marketing Team